Air freight rates from Asia appear to have peaked for now but will remain elevated for some time, with the constrained capacity and inflated rate situation not expected to change drastically in 2022, according to European freight forwarder Scan Global Logistics (SGL).

SGL’s latest Market Outlook Advisory highlighted that the recent online shopping sales season and the traditional Christmas rush have been causing constraints on most of the major trade lanes, with Asia to the US and Asia to Europe — as usual, the most impacted ones — having experienced a significant increase in rate levels. Other trade lanes, such as Europe-Asia, Europe-US, and Latin America, «remain under strong pressure too, albeit with a lower degree of rate increase impact», the Denmark-based forwarder underlined.

It noted that recent weeks and months had highlighted the importance of airport cargo ground handling agents (GHAs), where Covid-related factors «across most airports have significantly impacted the industry, causing backlogs and bottlenecks to which there is no quick-fix solution. The cocktail of labour and equipment shortage, warehouse congestion, and increasing pick-up/delivery waiting times will continue to cause delays for the foreseeable future.»

Asia exports

But SGL said the highest focus, «as is often the case», is on exports from Asia, where «increasing cargo output and capacity constraints continue to put high pressure on rates and transit times». It said passenger flights «are only resuming at a very slow pace, and we do not expect a significant effect from this in the short term. In fact, some signs of an increased level of restrictions could cause the suspension of certain flights again.»

SGL observed: «The rates we currently see in the market to and from Asia will remain elevated. However, our assessment is that the peak has been reached for now.»

SGL highlighted continuous pressure on transatlantic capacity as well, even with travel restrictions lifted to the US. «Several airlines have announced an increasing number of flights over the coming weeks and months but it is expected that it will take time for this to ramp up. Also worth noting is that an increase in passenger travel could have a short-term negative effect, leaving less room for cargo payloads from a total weight perspective.»

Wider outlook

SGL expects most trades «will only experience a moderate development until the end of the year, implying that rates will remain elevated. Looking into next year, we do not assess that the capacity and rate situation will change drastically in 2022. Additional passenger flights will positively impact the capacity side, but as mentioned, the decrease in payload versus pure cargo flights will negatively balance this effect. However, frequencies and the number of served (air)port-pairs will undergo a positive trend.»

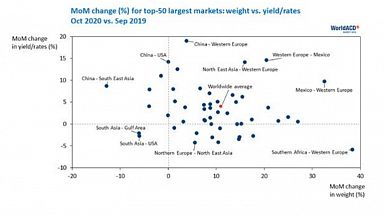

SGL said the current market situation is clearly explained in Clive Data Services’ October market update, which highlighted that with a 13% reduction in capacity versus 2019 and a 3% increase in volumes, the global load factor remains high. «Especially on the largest trade lanes, we see an even higher impact between supply (available capacity) and demand (transported volumes).»

Lastly, a very strong indicator that air freight rates will continue at an elevated level is the «implosion» in the air and ocean rate differential on a per kilo basis, SGL observed — from a price differential of around 13:1 in September 2019 to less than 4:1 this year. «With such a slim price differential versus ocean freight, it is our clear assessment that the demand for air freight will remain red hot, overall sustaining the current market situation,» SGL said.

It concluded: «Increasingly, we experience customers that are looking into full charters in order to evacuate products from Asia. This is a viable option, albeit also a costly one due to limited aircraft availability.»

US forwarder Flexport last week reported that air freight’s Far East westbound ‘super-peak’ season was set to last until Chinese New Year and said that with little prospect of an improvement in capacity on the horizon, any significant change in the current elevated level of rates is unlikely. And the UK’s Metro Shipping this month Metro highlighted that «predictions are that the air cargo boom will continue well into next year, and possibly 2023, as it may take that amount of time for the passenger schedule to return to pre-COVID levels».

IATA predicted in July that global air passenger traffic will not return to pre-Covid-19 levels until 2024, a year later than it had previously forecast.