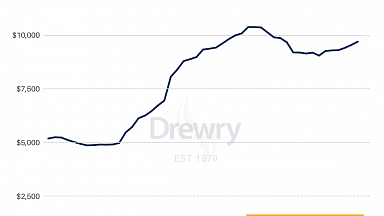

After 22 consecutive weeks of increases, Drewry’s World Container index (WCI) composite index stopped its seemingly inexorable rise this week, a possible early indication that ocean freight spot prices may finally have peaked.

The WCI index — which is a composite of container freight rates on eight major routes to and from the US, Europe and Asia — remained steady this week at $10,377.19 per 40ft container, but is nearly four times the level (299% higher) than the same week last year, the container shipping analyst reports.

Rates on Shanghai to Rotterdam, Rotterdam to Shanghai, Shanghai to Los Angeles and Rotterdam to New York remained stable at the previous week’s level.

Drewry highlighted that this flattening of spot prices «comes following the announcement by CMA-CGM and Hapag-Lloyd to put a halt in increment of spot rates, as container prices on most trade lanes are at record highs».

Freight rates on Shanghai to Genoa gained 1% or $144 to reach $13,646 per 40ft box. However, spot rates from New York to Rotterdam dropped 8% or $91 to $1,107 per feu. Similarly, rates on Los Angeles to Shanghai and Shanghai to New York fell 3% and 2% to reach $1,404 and $15,849 per 40ft box respectively.

![]()

Drewry said it expects rates to remain steady in the coming week.

Freightos also noted a flattening in prices this week, judging that in part this was due to lowered risk of disruption from Typhoon Chenthu as the weather system — «which had the potential to be the latest cause of the string of logistics disruptions in China this year — shifted east before making landfall near Shanghai last week».

Freightos’ head of research, Judah Levine, commented: «With the potential crisis averted, and with the recent cap on spot rates from some carriers in place, ocean rates were stable overall this week, with Asia-US West Coast rates even declining slightly.

«But transpacific demand remains in high gear, and carriers continue to add capacity in response. To do so when basically all of the globe’s container ships are already active, carriers are moving capacity from secondary lanes to the transpac, complicating things for shippers on those lower-profile routes.»

Levine highlighted research indicating that there are about 40% fewer ships servicing the Asia-Middle East lane than originally scheduled, «and transatlantic rates have increased 16% so far this month to a record high quadruple its level a year ago».

He added: «Unfortunately, that transpacific capacity is increasingly stuck waiting at US destinations like LA/Long Beach. Though the main West Coast gateway announced extended gate hours for trucks to collect containers and speed operations, a new record of more than 70 ships are currently waiting an average of nine days for a berth to open up.»

Overwhelmed trucking, warehouse and rail logistics are also contributing to the port delays, «and to the overall slog in end-to-end logistics», Levine noted, adding: «Freightos.com marketplace data shows that so far this month China-US ocean shipments are taking an average of 73 days to arrive at their final destination, 83% longer than in September 2019.»

Levine continued: «Durations like those mean that, with the holidays rapidly approaching, goods that don’t ship soon may not make it in time. This pressure is adding to the trend of ocean to air conversions which, together with COVID restrictions and air cargo capacity constrained by the lack of passenger jet activity, are pushing air cargo rates in and out of Asia ever closer to the highs only seen during last year’s rush on PPE.»