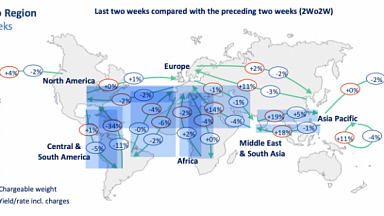

Global airfreight rates cooled sequentially over the course of January — especially on North America-bound Transpacific routes — as a protracted and robust peak season wound to a close, according to the Baltic Air Freight Index (BAI) but on a multi-year stack, remain well above historical peaks.

Its latest monthly analysis showed that prices on the Shanghai to North America ’basket’ have declined nearly 40% since the start of the year, although this is probably of little solace to shippers who paid more than double for the same capacity on that route in January 2021 compared to January 2020.

Commenting on the the BAI’s findings, Bruce Chan, vice-president and senior analyst, Global Logistics & Future Mobility Equity Research, at investment bank and financial services company, Stifel, noted: «While there was some sequential easing of airfreight rates as we moved deeper into a typical seasonal first-quarter lull, the data shows unusual volatility. And there is evidence that absolute rates are ticking back up again on certain core lanes. This volatility and uncertainty are exacerbating challenges for shippers and will require new approaches to supply chain planning and budgeting, in our view.»

’Long term capacity constriction’

Chan continued: «The unfortunate news for end-purchasers of capacity is that we see availability remaining a constraint for some time. Consensus is pointing toward a pickup in passenger flight traffic towards the back half of the year as vaccines are disseminated, but that is heavily weighted towards short-haul, domestic leisure lanes, in our view. Long-haul travel, which is a much bigger part of global air cargo capacity, should be slower to resume. Our baseline assumption is that the market will not be back to normal until 2023.

«We’ve seen some incremental freighters coming into the market. And the current pricing environment is changing operator pain tolerances for feedstock that may have been considered prohibitively-expensive just a year ago. But production and conversion lead times are high, and the outlook for the industry and global economy is not free from uncertainty. Both factors are headwinds to augmented freighter capacity.»

Charter usage more ’mainstream’?

Consistent with Stifel’s view toward long term capacity constriction, Chan underlined that a number of large freight forwarders have articulated that charter will become a more permanent part of their service offerings. He added that if and as charter usage becomes more mainstream, there may be some practical competitive implications.

«Namely, a market that prefers large players with density and economies of purchasing scale and scope. This trend likely accelerates consolidation that was already occurring around players with technology, sophistication, and global network differentiation. It also means that total average airfreight rates are likely to stay higher for longer. And it may further separate the shipper ’haves’ from the ’have nots’ - that is, shippers with high-enough margins that airfreight rate increases are not as proportionately detrimental. We assume that any shipper that was on the fence about the airfreight cost-benefit tradeoff has firmly picked a side at this point.»

Structural changes

It is not just pandemic disruption and post-Covid restocking that are affecting capacity and pricing dynamics, Chan observed. The e-commerce megatrend and supply chain regionalization are altering demand cycles and routes.

«Rapid replenishment, quick lead times, and a distributed fulfilment center network mean that belly space, which is intrinsically attached to passenger flight gateways, may not be the most efficient and effective source of capacity. Rather, all-cargo or charter flights to secondary gateways are becoming more common, in our view.»

He concluded: «In short, the absolute rates that we have been tracking in the Baltic Air Indices may stick around longer than expected and may be more volatile than expected. But even as we move beyond the pandemic, structural changes to the air cargo market, its constituents, and consumers may signal a higher new normal for rates.»