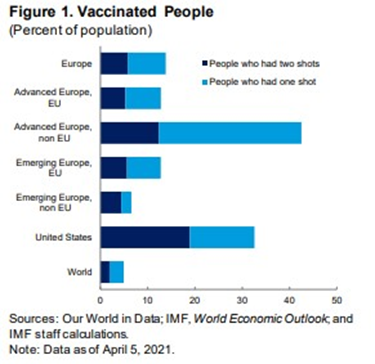

The coronavirus disease (COVID-19) pandemic continues to pose extraordinary challenges. New waves of infection have afflicted advanced and emerging European economies. Vaccination, a game changer, is under way but the pace of progress is still moderate and varies significantly across countries, with the biggest lags in several non-EU emerging European economies.

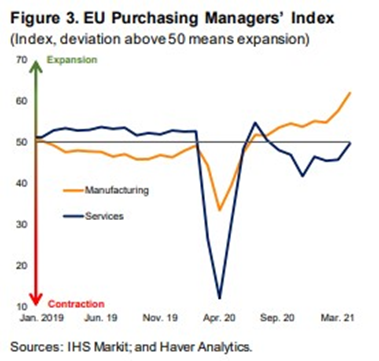

The recovery remains uneven. While industrial production has returned to pre-pandemic levels, services are still contracting. Accordingly, the recovery in countries with sizeable service sectors (for example, Croatia, Italy, Montenegro, Spain) lagged the rest of Europe by about 1 percentage point in the second half of 2020.

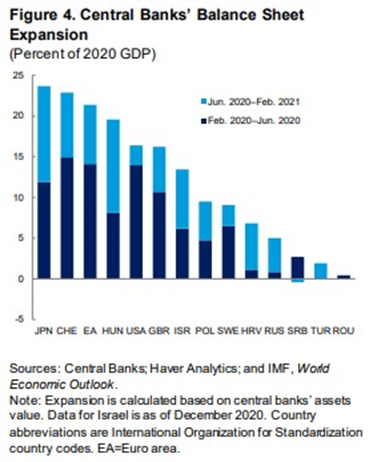

Several central banks cut policy rates further (for example, Iceland, Moldova, North Macedonia, Romania, Serbia); the exception was Russia, which has hiked rates reflecting higher-thanexpected inflation. Turkey has also hiked rates in response to foreign exchange and inflation pressures, reversing its strong monetary stimulus in 2020. Central banks also continued implementing unconventional monetary policies.

The European Central Bank increased the pandemic emergency purchase program by €500 billion to €1.85 trillion and extended the targeted longer-term refinancing operations to mid-2022. Central banks in emerging European economies (Hungary, Poland, Romania, Turkey) continued to expand their balance sheets in various ways. As a result, financial conditions remain highly accommodative. The announcement of US fiscal stimulus has so far had limited spillovers on European yields.

Europe’s GDP is expected to rebound by 4.5 percent in 2021. This is 0.2 percentage point less than forecast in October 2020, reflecting the new COVID-19 waves and lockdowns. On the assumption that vaccines become widely available in the summer of 2021 and throughout 2022, GDP growth is projected at 3.9 percent in 2022, bringing Europe’s GDP back to the prepandemic levels. Long-term output losses relative to the pre-COVID-19 trend are projected at about 1.5 percent of GDP by 2025. However, these projections are likely to change as the full impact of the pandemic on the economy becomes clearer.

Inflation, currently contained by economic slack, is projected to edge up by 1.1 percentage pointsto 3.1 percent in 2021, partly due to higher commodity prices. Inflation expectations remain around or below targets, not least reflecting the strong credibility of major central banks, although they have risen from their historical lows in the euro area.

The full version of the article is available here.