Introduction

Against a backdrop of increasingly difficult economic and political relations, COVID-19 diplomacy and the impact of the US–Chinese trade dispute, the EU can no longer prevaricate in its approach to China. The country has become not only a foreign and economic policy challenge, but also a source of disagreement in the transatlantic relationship. While European policymakers and business leaders share many of the gripes that their American peers have uttered about Chinese economic practices, they lack an agreed common strategy for how to deal with these.

The economic relationship remains the main lens through which the EU views China. European businesses and many governments have seen, and still see,

the Chinese market as an opportunity, owing to the country’s size and growing income levels as well as its role as ‘Europe’s producer’. The economic relationship is also defined by the geopolitical context. This became clearer at the end of 2020 when the EU’s conclusion of a Comprehensive Agreement on Investment (CAI) with China created a first point of contention with the incoming US administration and led to some tension among member states.

This paper is the first step in the Transatlantic Dialogue on China to facilitate exchange between the US and Europe on economic issues related to China. Given the rapidly shifting context, the increase in tensions between Europe and China, and the uncertainty over US policy on China under the Biden administration, it looks at EU policymaking on China to provide a clearer view of its direction and priorities. The paper describes how the EU and its member states see the economic relationship with China and how this is likely to develop in the context of the US–China rivalry.

Economic context

EU member states have different bilateral economic relationships with China, often reflecting the nature of their own economies. Understanding these differences provides a perspective on the incentives each country faces in its political interactions with China and with the EU. Countries with deep trading relations with China, particularly those with large export dependencies or those that have invested significant amounts of money there, have potentially strong domestic constituencies with an incentive either to favour a soft approach towards China or to use economic tools in an attempt to influence its policies.

Trade

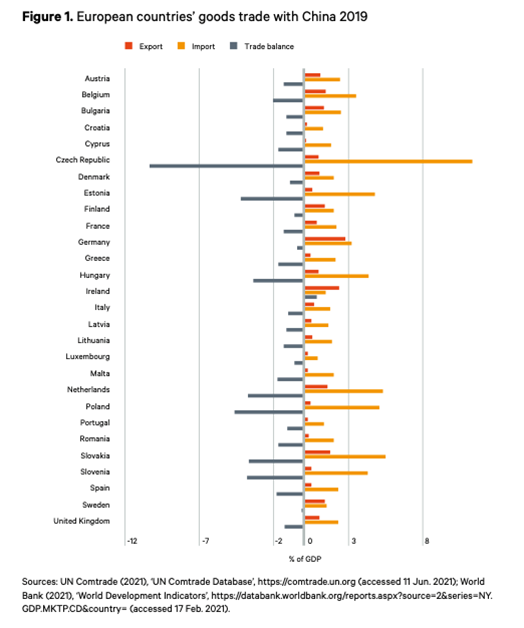

All European economies have a substantial dependency on imports

from China. This increased across the continent as manufacturing shifted to the country, particularly following its accession to the WTO in 2001. All European countries import significant amounts of goods from China, with Central European countries and those serving as ports for the rest of Europe, in particular Belgium and the Netherlands, standing out (see Figure 1).

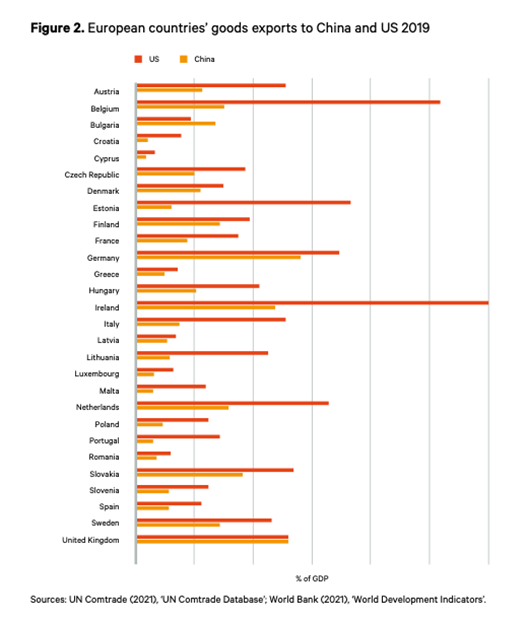

Continued growth in imports from China even during the COVID-19 crisis suggests this is not likely to change anytime soon. Goods exports from European countries to China remain a lot more modest, with those from Germany the only notable exception. As a result, all EU member states run trade deficits against China. This is in sharp contrast to their trade relationship with the US, with each country still exporting significantly more to the US than to China (See Figure 2).

Investment

Chinese FDI in Europe has been unevenly distributed, with a focus on Western Europe. Until recently it was also small, in line with Chinese FDI in general

(see Figure 4 below). A surge in 2016–17, combined with increasingly ambitious Chinese rhetoric on the country becoming the global leader in several high-tech manufacturing sectors, caused concern that this investment was being used to acquire technology with the aim of eventually outcompeting European producers, as part of the Made in China 2025 strategy. Since then, FDI from China has decreased but the issue remains on the radar of policymakers. For most European countries, Chinese investment makes up only a negligible share of all FDI and in most cases is dwarfed by US FDI.

Technology

Despite its dependence on imports from China, the European economy is still more reliant on the US. Almost all European countries export significantly more to the US than to China and the economies of Europe and the US are deeply intertwined through extensive investment relations. Western European countries have a long history of deep economic and political integration with the US. Although transatlantic tensions have increased in recent years, and were exacerbated by the Trump administration, the US–EU connection remains close. This stands in sharp contrast with Europe’s relatively new relationship with China, which focuses mainly on trade and for some countries on investment. One of the sectors where this is most visible is in technology.

The elephant in the room

By almost all measures, Germany has a deeper economic relationship with China than any other EU member. The value of German goods exported to

the country in 2019 was equal to the combined exports to China of all other

EU members, driven by Chinese demand for German capital goods, machinery and cars. This is also a reflection of the size of the German economy and its export dependence. Exports to China were equivalent to 2 per cent of Germany’s GDP and made up 8 per cent of its exports. This was slightly higher than exports to the UK but still below those to the US.14

European issues with China

Many European countries have primarily viewed relations with China as an economic opportunity. Following its entry into the World Trade Organization (WTO) in 2001, China was seen as a source of cheap manufacturing imports

and as a destination for investment in manufacturing industries. While the

extent of the latter differed significantly between countries, the former was true across Europe, and in line with views of other developed countries. As China developed, however, it also provided the lure of potentially the largest market of middle-class consumers for European businesses. At the same time, the implicit assumption behind much EU policy in recent decades was not only that China would converge economically with the West, but also that this would facilitate political convergence.

Market access

European businesses and policymakers have long been frustrated by limited market access in China. Many sectors have either not been open to foreign companies or only accessible through joint ventures with local partners. In the latter case, this often involves the forced transfer of technology as the price

of doing business. There have also been related complaints over the protection of intellectual property in China and over requirements for participation

or surveillance in companies by the Chinese Communist Party.

Chinese competition

The operating environment for companies in China is not the only issue for the EU. Governments also worry about the impact of Chinese operations in Europe and increasing competition from Chinese firms, often on what many policymakers and business representatives judge to be an unfair basis. This ranges from technology transfer through acquisitions of European firms to distortions of the single market through non-market support for firms with Chinese ownership and dumping of Chinese products. In recent years, a slowdown in Chinese FDI and the beefing up of investment-screening mechanisms throughout Europe have slightly reduced the urgency of this issue. Nevertheless, China has moved up the agenda for many European countries as it is increasingly seen as an economic competitor.

Politics complicating mercantilism

Political disagreements between the EU and China complicate their economic relationship and this worsened as tensions between the two increased in the first half of 2021. European political leaders and civil society actors have long voiced concerns over the lack of democracy and respect for human rights in China. Developments in recent years have intensified these concerns as the treatment of ethnic minorities in Xinjiang and the crackdown in Hong Kong made headlines in the West. These issues may prevent both sides continuing along the well- trodden economic track as European civil society and parliaments have become increasingly vocal in their criticisms of Chinese actions. The perceived mishandling by China of the initial phase of the COVID-19 pandemic also led to a rise last year in unfavourable views of China across Europe. As a result, several European firms have come under public and political pressure over their operations in China. Relations between European countries and China worsened further in 2021 following the imposition of sanctions by the EU on a number of Chinese individuals connected to alleged human rights violations in Xinjiang. China responded with countersanctions, leading to the ratification of an already agreed investment agreement between the EU and China being put on hold (see below).

Formulating China policy in the EU

The EU’s foreign economic relations are to a large extent governed at the union level. As a result, its approach to China requires the approval of disparate countries with different economic interests, threat perceptions and assessments of the urgency of the issue. That the differing national perceptions of the economic threat posed by China have changed only relatively recently has probably contributed to the fact that there is still no comprehensive EU China strategy. Despite the sizeable and increasing number of complaints about China, no coalition or member state has pushed for a more confrontational line. In 2019, the European Commission published a strategic outlook document, describing China as a partner, an economic competitor and a systemic rival. The latter term grabbed the headlines, but member states have been slow to use this more confrontational definition. They have to some extent left this to the European Commission, in part because it allows them to disavow any stronger language coming from Brussels when necessary. In that regard it was telling that the European Council did not specifically endorse the strategic outlook document in its subsequent meeting.32 Basically all member states are pursuing what they consider a pragmatic policy towards China, considering it both a competitor and a partner.

The EU’s China policy

Since economic interests drive EU policymaking towards China, especially

in trade and investment, some member states are more prominent and engaged in the process than others. The EU, and in particular Germany, continues to see potential benefits from China’s economic rise. The EU’s overall economic policy response to the challenge China presents effectively consists of a set of defensive and mercantilist economic policy measures, which are guided by a broader geopolitical vision of the EU as a neutral actor between the US and China.

Pursuing strategic autonomy

The combination of a mercantilist approach to China, including attempts to

gain small concessions from it on market access, and a focus on protecting the integrity and strength of the single market is in part informed by the geopolitical assessment made by European leaders. A long process by the US of shifting its foreign policy focus from Europe towards Asia, symbolized by the ‘pivot’ under the Obama administration, was followed by the Trump administration’s actions that deeply undermined European trust in the transatlantic relationship. The latter included threats from Trump to withdraw the US security guarantee for Europe and a low-level economic conflict through the imposition of tariffs. These, and in particular the threat of tariffs on German cars, confirmed for Chancellor Angela Merkel that ‘the era in which we could fully count on others is somewhat over’.40 Meanwhile, for France, which has always seen the EU as a lever for its own influence in the world, this reinforced the importance of building a more independently capable EU in geo-economics and security.

The China toolbox

In response to its market access and competition considerations the EU has in recent years built up a toolbox of mainly defensive economic policies. Although

not explicitly in response to China, its framework for screening FDI, which became operational in late 2020, features prominently among these measures. The main aim of the framework is to enable better information sharing on foreign investment screening, which is still done through national instruments, and it allows the European Commission to submit an opinion in certain cases.45 Another modest instrument is the 5G toolbox introduced in early 2020 in response to member. states adopting differing lines towards the inclusion of Huawei in their respective 5G rollouts. The toolbox incorporates measures that member states can use to ensure a coordinated approach to the security of 5G networks but does not exclude Huawei involvement. In mid-2021, the European Commission put forward a proposal for a regulation to tackle distortions of the level playing field that arise from subsidies provided by foreign governments to firms operating within the single market. These specific instruments all complement existing trade defence instruments such as anti-dumping and anti-subsidy measures. The EU also considers its efforts to reform multilateral systems, such as the WTO, as part of this approach. As in the past, it hopes to use these mechanisms to exert pressure on China to comply with the rules of the multilateral trading regime.

A risky strategy

The many small measures in the EU’s toolbox should partly protect the single market from distortions resulting from China’s economic model. However,

in most cases their impact is likely to be limited. For instance, investment-screening relies on member states to use their national policy mechanisms, which some lack beyond tools aimed at industries such as defence.50 Deep divisions remain within the EU over the direction of its industrial policy, with the Franco-German proposal for reform yet to be followed up. The introduction of the 5G toolbox did not lead to a common approach, with some countries having effectively banned Huawei from their 5G networks while others, notably Germany, look set to effectively allow it. A new instrument to counter foreign subsidies might be effective but would, at best, counter a relatively small problem. Efforts to reform the multilateral trading system through the WTO and use this to influence Chinese economic and trading practices are also likely to prove difficult, as similar efforts have been largely unsuccessful for decades and face structural obstacles. Even if many of these measures achieve their intended effect, they would still constitute a strategy reliant on incremental policy changes.

The CAI case study

Many of the issues discussed above, including German dominance in the EU’s China policy and the interplay between economic objectives and political barriers, were prominent in the EU’s attempts to conclude an investment agreement with China, the EU–China Comprehensive Agreement on Investment (CAI). The CAI has the potential to support further European investment in China by opening up several sectors and easing restrictions on EU companies operating in China. From the EU perspective the aim is to ensure a level playing field with American firms that received some of the same access through the agreement that the US and China reached in early 2020, and to compete with Chinese companies. However, significant uncertainty remains over whether this will happen, not least as the CAI still needs to be approved by the European Council and the European parliament. The agreement would in any case be likely to benefit those member states that are already heavily invested in the Chinese economy. German firms, particularly in manufacturing and the automotive sector, once again stand to benefit from the loosening of foreign ownership restrictions. It was therefore not surprising that Germany, together with France, was among the driving forces getting the agreement over the line in late 2020. Some smaller member states objected to this, but not enough to derail the process.

Transatlantic cooperation

The change of US administration in 2021 offers more room for EU–US cooperation on China. In their confirmation hearings, Secretary of State Antony Blinken and Trade Representative Katherine Tai spoke of the US relationship with China as having adversarial, competitive and cooperative aspects – similar to the EU’s assessment of its own relationship with China. The Biden administration has also been vocal about its wish to work with allies on China and other global challenges, in contrast to the Trump administration. At the same time, an assertive US approach to China retains bipartisan support.

Summary

EU–China relations have become increasingly strained in recent years.

For the most part, the EU’s approach to China has been driven by the economic interests of a small number of member states, but relations are becoming more complicated. Internal and external political tensions make doing business in and with China even more difficult, while the country’s emergence as an economic competitor has reinforced the EU’s insecurities about its own future economic position in the world.

China’s heated rivalry with the US has also become an issue of contention in the transatlantic relationship, despite the EU having similar and growing frustrations over China. The Biden administration is keen to work with allies in dealing with China and the EU has so far suggested a limited willingness to do so.

Beyond developing a toolkit of small, largely defensive measures, the EU’s approach to the economic challenge from China, as well as to broader geopolitical and geo-economic issues, has been to pursue ‘strategic autonomy’. It aims to be a neutral, but not equidistant, third pillar in a world order dominated by China and the US.

This is a risky and largely unsustainable strategy. If not followed through with enough conviction, it could result in continued soft triangulation and less effective attempts to profit economically. The EU will remain vulnerable to economic and political pressure from both the US and China, as demonstrated in early 2021 when China imposed sanctions on several European actors and the US threatened to impose sanctions and tariffs on several member states.

The investment agreement that the EU concluded with China at the end of 2020 highlights many of the difficulties in current European China policy. Attempts to reap the benefits of deeper economic engagement with China led to political tensions with the US. Subsequent mutual imposition of sanctions between the EU and China delayed or halted ratification of the agreement and highlighted the difficulty of separating the economic and political spheres.

Meaningful transatlantic cooperation on China is limited by fundamentally different EU and US views on several issues. This includes whether to take a confrontational or mainly defensive approach to China. It is also affected by the fact that much of the EU autonomy and sovereignty agenda has been developed with an eye more on the US than on China. Nevertheless, there is room for cooperation in several policy areas and the change of administration in the US provides an ideal opportunity to pursue this.